Instrument Failure

A Formula 1 steering wheel is only useful when you can trust what it's telling you. Today's bond markets are presenting the same problem.

Mohamed El-Erian — former CEO of PIMCO, chair of Gramercy Funds, counsel to governments on six continents — is also someone Paul Pfanner knows from the sideline of an AYSO soccer field in Laguna Beach, where they spent weekend mornings cheering their daughters through games. This week El-Erian posted something on LinkedIn that he himself called understated. An AI synthesis of the past 24 hours of market commentary elevated it — in his own words — to something considerably more alarming. After fifty years of launching businesses directly into recessions — four of them, plus a pandemic — Pfanner has learned to take early signal seriously before it gets loud. He's inclined to agree. This is the column that followed.

Mohamed El-Erian called his own post understated. An AI synthesis of 24 hours of market commentary called it considerably more alarming. He agreed.

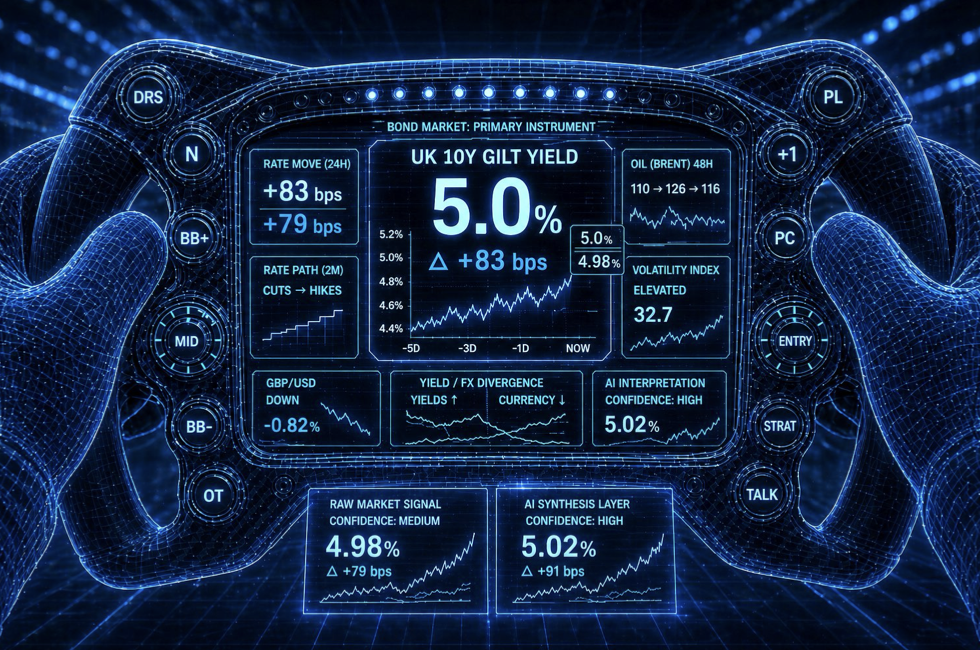

Earlier this week, Mohamed El-Erian posted on LinkedIn that UK 10-year gilt yields had breached 5% — and noted that an AI-generated review of the past 24 hours of market commentary had taken his own "understated" framing to what he described as "a much more alarming level." He drew on other signals: Brent crude climbing, the Iran blockade threatening further energy disruption, the historical precedent of October 2022, when gilt volatility of this magnitude took down a Prime Minister in 44 days. His conclusion was precise and carefully worded: the conditions for a sovereign debt stress event are quietly assembling.

I am not a financial journalist. But my sister Dianne spent years as a global asset manager for BP, based in London. I worked for Michael Heseltine and Haymarket, with frequent visits to HQ in that same city. I have watched London's financial and political architecture from close range — and I have watched it under stress. That was a long time ago. But pattern sensitivity doesn't expire. When someone I trust reads the instruments and says something is quietly assembling, I have learned to look up.

The Canary Is Already in the Shaft

The yield has surged more than 80 basis points since the US-Iran conflict began in late February — crossing 5% today for the first time since 2008 — and the volatility in shorter-term gilts now matches levels last recorded in October 2022, when a single British budget announcement — Liz Truss's ill-fated mini-Budget — ignited a market fire that burned down a Prime Minister in 44 days.

That episode is the historical marker that makes serious people nervous. It demonstrated something the textbooks know but politicians routinely forget: bond markets are not audiences. They are referees. They don't applaud or boo. They simply move the goalposts — and when they move fast, careers end and policies collapse overnight.

The question El-Erian is raising is whether what is assembling now is a replay of 2022, or something considerably larger.

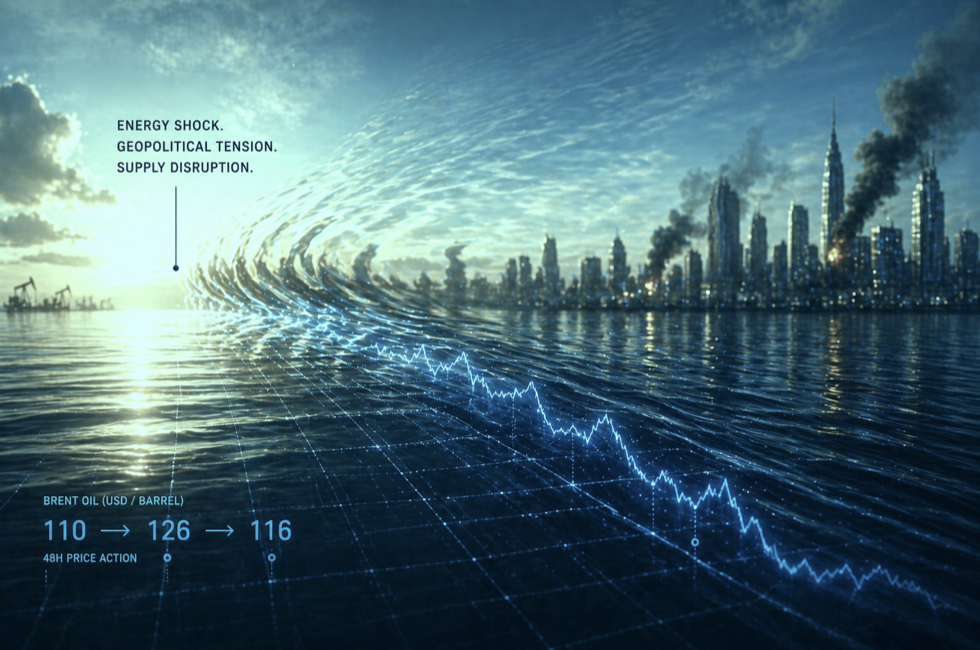

Brent crude moved from $110 to $126 and back to $116 in 48 hours. The ripple doesn't stay where it starts.

Three Fires, One Room

The argument runs like this. A sovereign debt stress event doesn't require a single catastrophic cause. It requires the simultaneous convergence of pressures that individually look manageable and collectively become overwhelming. Right now, three fires are burning in the same room.

The first is energy. In the past 48 hours, Brent crude swung from $111 to a high of $126 before pulling back to $116 — a $15 range in two days that El-Erian described as "far from cost-free for the global economy." The pace is the signal, not just the price. American drivers are already absorbing the consequences: the national average for regular gasoline has crossed $4.23, up from $3.16 a year ago. El-Erian noted this carries weight "far beyond economics, especially with political and social dimensions." The UK's dependence on imported gas means the pass-through to households and firms is even more direct — and faster.

The second is fiscal fragility — and it just got a global dimension. At the start of 2026, markets anticipated three Federal Reserve rate cuts before year's end. As of today, traders have completely priced those cuts out. In their place: expected rate hikes — not just from the Fed, but from the Bank of England and the European Central Bank simultaneously. That is a synchronized global tightening cycle nobody planned for, arriving on top of a war, an energy shock, and sovereign debt loads that were already at historic highs. For the UK specifically, the pre-conflict Office for Budget Responsibility had projected roughly £109 billion annually in debt service costs. That number is now moving sharply in the wrong direction at precisely the moment the government faces pressure to spend more to cushion households from energy prices. Chancellor Rachel Reeves has staked her credibility on fiscal discipline. Bond markets respect that — until they don't. The margin for error has narrowed to almost nothing.

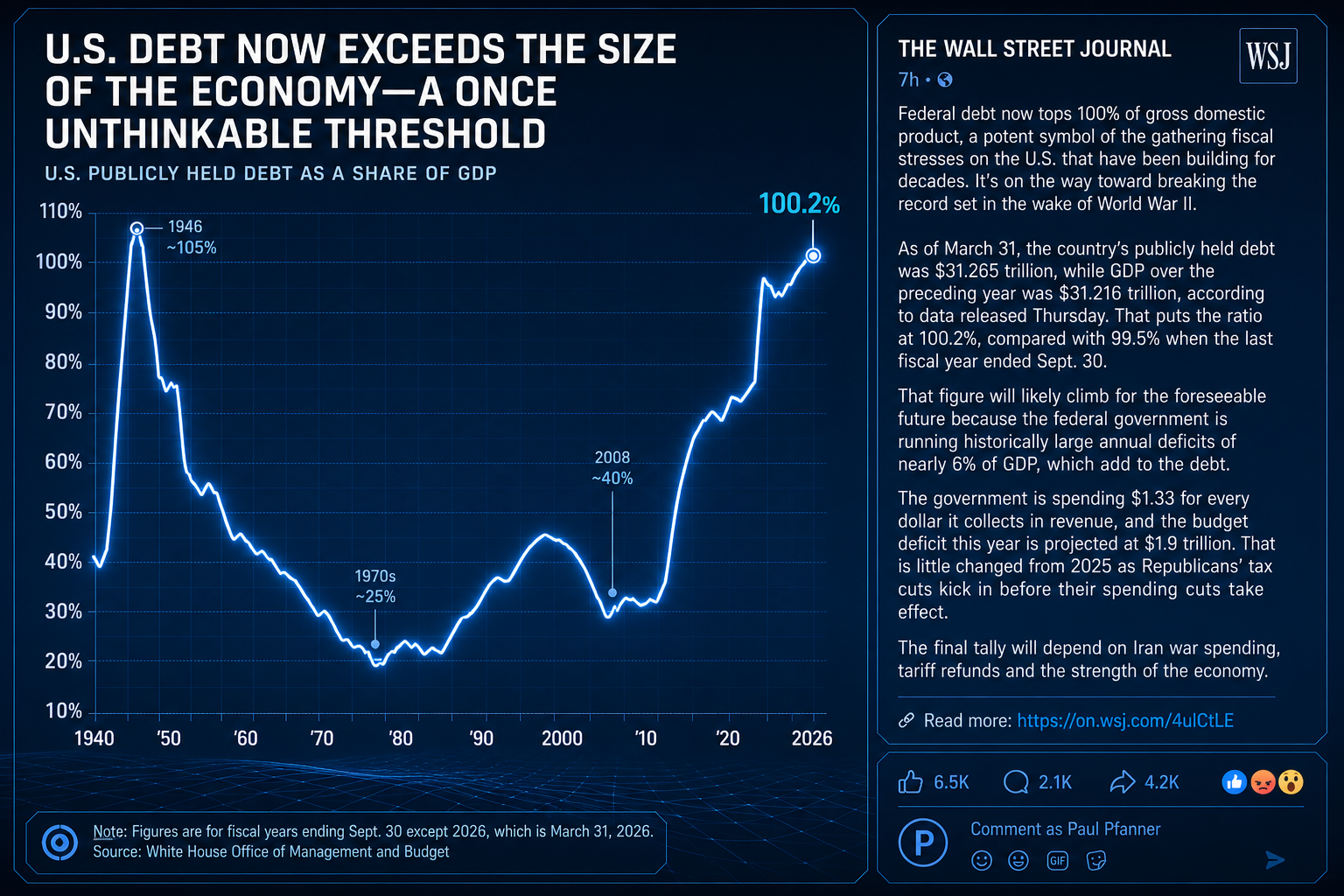

US publicly held debt crossed 100% of GDP this week for the first time since World War II. Then, it was financing a war. The current explanation is less heroic. Chart: The Wall Street Journal / White House Office of Management and Budget.

The third is political noise. Betting markets currently place roughly even odds that Keir Starmer will no longer be Prime Minister by summer. Local elections loom. Internal Labour politics are messy. And investors — especially the overseas capital that now plays an outsize role in the gilt market — price political instability into sovereign debt with brutal efficiency.

Individually, any one of these pressures is manageable. Together, they rhyme with 2022 in uncomfortable ways. I have spent fifty years watching markets, industries, and institutions under stress. The pattern I keep returning to is simple: everything is connected.

What the Instruments Are Telling Us

Here is what I find most instructive about El-Erian's post — and why I'm writing this today rather than waiting for things to get clearer.

He didn't say the UK is collapsing. He said the conditions for a sovereign debt stress event are quietly assembling.That is signal language. It is the vocabulary of someone watching the instrument panel, not the grandstands.

In motorsport, the most dangerous moment on a race track is not the obvious wreck unfolding in front of you. It's the vibration in the steering wheel that started two laps ago — the thing you noticed but haven't yet named, while everything still looks fine from the grandstands.

Bond markets work the same way. By the time the crisis is obvious, the opportunity to respond to it has already passed. The 2022 gilt crisis didn't happen on the day Truss resigned. It began assembling weeks earlier, in the quiet mispricing of assumptions that seemed reasonable right up until they weren't.

El-Erian is reading the vibration. That's worth paying attention to — because what happens to UK borrowing costs doesn't stay in the UK. A reassessment of policy credibility in one major economy tightens financial conditions globally, pushing yields higher across the system even in countries with sound domestic policy. The initial disturbance need not originate in the country that ultimately suffers most.

Why This Is a Motorsport Story

Bond markets are, in a very precise sense, the timing system of the global economy.

When a race team's timing system fails, nothing else works correctly. Pit stop windows get missed. Strategy calls get made on false data. The car that looked competitive at lap 30 turns out to have been running on borrowed time.

A sovereign debt stress event is a timing system failure. It doesn't destroy the underlying economy directly. What it does is remove the instrument panel that everyone — governments, businesses, households — depends on to make decisions. When you can no longer trust the cost of money, you can't plan. When you can't plan, you stop. And when enough actors stop simultaneously, the thing that was manageable becomes unmanageable very quickly.

When the Pound Starts Behaving Like the Peso

There is a signal embedded in the gilt crisis that hasn't received enough attention outside professional finance circles, and it is the one that concerns El-Erian most at a structural level. In a healthy sovereign debt environment, when a country's bond yields rise sharply, its currency typically strengthens — investors are, after all, demanding more return to hold that country's assets. What is happening in the UK is the opposite. Sterling is falling at the same time gilt yields are rising.Yields up, currency down. That is not G7 behavior. That is the signature pattern of an emerging market under stress.

Sterling is not alone. The Japanese yen crossed 160 to the dollar yesterday — a threshold that triggered what El-Erian called a "game of chicken" between FX traders and Japanese authorities. The Ministry of Finance and the Bank of Japan intervened verbally to push it back below 160. It worked, briefly. But the fact that Japan's policymakers are already in verbal intervention mode is itself a signal. When the world's third-largest economy is defending its currency in real time, the stress is not contained to one country or one market.

The implications of both travel directly to the US dollar. When major developed-economy currencies behave like distressed assets simultaneously, global capital has one reliable refuge: dollar-denominated instruments. That flight to the dollar tightens financial conditions everywhere — not just in the UK or Japan, but across every economy whose debt is priced in relation to dollar benchmarks. The dollar becomes more expensive precisely when the rest of the world can least afford it. Commodity-dependent economies get squeezed. Sovereign borrowers with dollar-denominated debt face rising repayment burdens. The feedback loop amplifies the original stress rather than containing it. This is the mechanism by which a gilt crisis and a yen crisis stop being local problems and become a global one — not through direct contagion, but through the currency system that connects every economy on the planet to every other one.

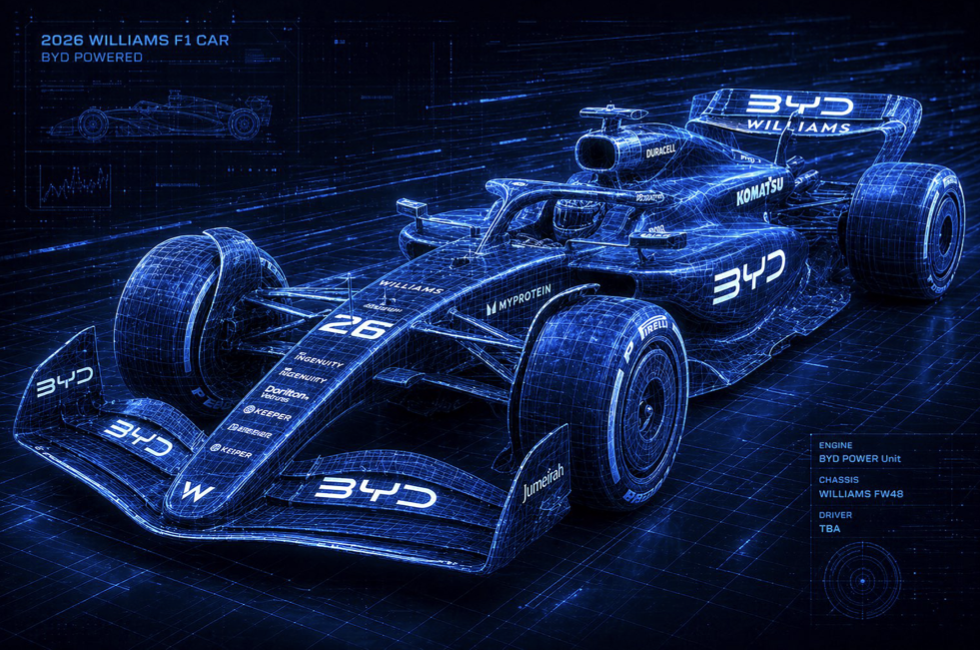

BYD at Williams isn't a sponsorship story. It's a market entry strategy — executed at the precise moment Western automotive capital is under maximum stress.

The Pit Lane Is Moving East

BYD has confirmed it is in talks to join Formula 1. BYD Vice President Stella Li described it as an opportunity to "put our technology to the test." BYD's executive vice president confirmed the company has been in contact with F1 leadership, including a meeting with CEO Stefano Domenicali in Shanghai. Williams Racing has emerged as a reported acquisition target. The financial barrier is real — establishing and running an F1 team costs upwards of $500 million per season — but BYD is not a company short of capital or ambition.

Read this as a market signal, not a motorsport transaction. BYD overtook Tesla as the world's largest electric vehicle manufacturer in 2025, delivering over 2.25 million battery-electric vehicles. Its overseas sales surpassed one million units for the first time, a 150% increase year over year, and the company is targeting 1.3 million units abroad in 2026. The F1 initiative is a brand-building move aimed at the premium global markets — Europe, Australia, eventually North America — where raw sales volume hasn't yet translated into the prestige BYD needs to compete at higher price points. It is, in the language of motorsport, a drafting move: get in behind the slipstream of a century-old sport's global credibility and use it to pull the brand into positions it couldn't reach through conventional marketing.

Here is what makes this directly relevant to the gilt crisis and the broader argument of this column. The global auto industry is being repriced right now — by energy costs, by supply chain disruption, by the rising cost of capital in exactly the sovereign debt environment El-Erian is describing. Western manufacturers are financing their EV transitions at borrowing rates that have doubled in three years. Consumer vehicle financing has become materially more expensive. The headroom that European and American automakers counted on for the capital-intensive shift to electrification is narrowing precisely as Chinese manufacturers — BYD chief among them — arrive with state-backed balance sheets, vertically integrated supply chains, and, now, a seat at the most prestigious table in global motorsport.

When the timing system of the global economy is under stress, competitive positions shift faster than anyone expects. The gilt crisis is one instrument. BYD at the F1 paddock is another. They are reading the same underlying signal from different angles.

I'll have considerably more to say about this in an upcoming column dedicated specifically to what Chinese manufacturers in global motorsport means for the industry, the sport, and the institutions built around both. That column is already writing itself.

What Comes Next

I'm not a macroeconomist. I'm not a bond trader. I'm a media founder and strategic advisor who has spent a career trying to read institutional signals correctly and early.

El-Erian called his own post understated. The market commentary that followed called it alarming. He agreed.

That's the instrument. It's vibrating.

Whether the next 30 days bring a resolution to the Strait of Hormuz crisis and a rapid reversal of gilt yields, or whether the conditions quietly assembling become something larger, I don't know. Nobody does. But the value of early signal is precisely that it arrives before certainty — and acts before certainty are the only ones that matter.

I have one other saying I return to in moments like this: the enemy of a lie is time. The lie right now is that these pressures are separate, manageable, and local. Time is already proving otherwise.

Victory travels at the speed of thought. In sovereign debt markets, so does collapse.

Pfanner Advantage works with clients to turn change into advantage at the intersection of mobility, motorsport, media, technology, and marketing. Learn more or start a conversation: contact us today.

The Advantage Journal arrives every week. What matters in sport, mobility, media, and technology — curated and contextualized by Bill Sparks, Bill Long, and Paul Pfanner. No hedging. No filler. Subscribe — It’s Free